The Human Cost: ‘2022 has been the scariest year of my adult and professional life’: One mortgage broker reveals how the housing slowdown upended financial security.

When mortgage rates hit 7% in the fall, Austin-based mortgage broker Aaron Kovac was a little spooked.

After a stunning rise in home sales amid ultra-low interest rates, “the market just went absolutely silent,” the 32-year-old, who has been in the mortgage industry for six years, told MarketWatch in an interview.

As the housing market slump drags on, fear has taken over. “This is my first time going through a decline in the real-estate market,” Kovac said, “2022 has been the scariest year of my adult and professional life.”

“It’s the same story everywhere — not just with other lenders, but also with real estate agents,” he added.

People in the real-estate industry are feeling the pain, as buyers stay on the sidelines, reluctant to buy homes. Meanwhile, rates remain firmly above 6%.

“If you were doing four to eight loans a month, you’re lucky if you have one or two right now. Many people that I’ve spoken to in the industry, including myself, have thought, ‘Do I get out? Do I need a second job to hold things over until the market picks up again?’” Kovac said.

And the stress from the dip in clients is weighing on his personal finances, and mental health, Kovac said: “All that uncertainty, wondering, where is my next paycheck going to come from? Where am I going to find that next buyer?”

Housing industry being ‘right-sized’

The real-estate industry is undergoing a major shift as rates spike, with lenders and brokerages trimming their staff to cut losses.

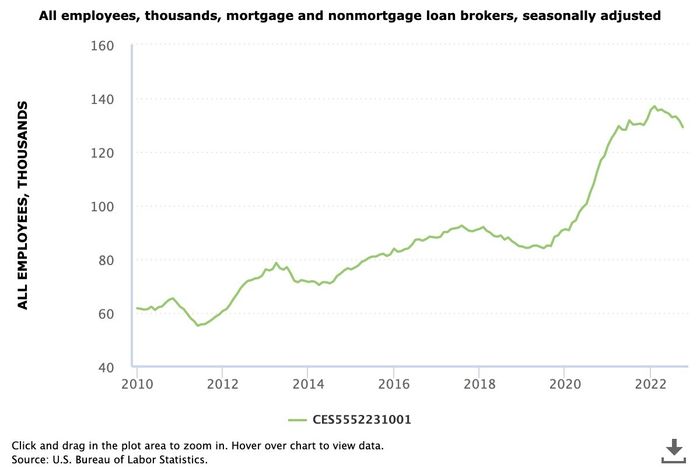

As demand surged, he number of workers in the mortgage industry also rose, as seen in the chart below:

The mortgage industry grew amid the pandemic, as rates plunged.

Bureau of Labor Statistics

But as rates rose and buyers backed off, conditions prompted re-sizing.

Real-estate brokerage Redfin went through two rounds of layoffs, in June and in November, reducing headcount by 27%. Compass, another brokerage, also laid off staff amid the housing downturn.

Lenders were also affected, from Better — which laid off 900 employees via a Zoom meeting — to Rocket Mortgage, which offered 8% of its workforce voluntary buyouts. JP Morgan Chase also laid off hundreds of employees in its home lending business. One Texas-based lender, First Guaranty Mortgage Corp., filed for Chapter 11 bankruptcy in June.

Given the drop in mortgage originations, the sector needs to shed roughly between a quarter to a third of jobs to “right-size the whole industry,” Mike Frantantoni, the Mortgage Bankers Association in industry group’s chief economist, told MarketWatch earlier this year. He also wrote an article about the numbers in August.

‘It’s like sharks smelling blood in the water’

For those working in the mortgage industry, like Kovac, the situation on the ground is tense, to say the least.

Being in Austin, a hot pandemic real-estate market, demand was strong over the last two years since mortgage rates were at record lows. In January 2022, Kovac said he locked in a mortgage for a buyer with a rate of 2.75% – the lowest this year he secured for a client.

But fast forward to mid-November, rates had jumped so much that clients weren’t happy: That month, he had closed a mortgage for a different buyer with a rate of 7.65%.

While these borrowers had different credit scores, amounts down for payment and such, hence had different rates quoted to them, the vast difference between the two was something out of Kovac’s hands.

At this point, lenders are scrambling to find business. “If there’s a buyer out there in the industry looking to buy, every lender is fighting over them and trying to go as low as possible,” Kovac said. “It’s like sharks smelling blood in the water right now.”

Kovac, who is a broker with Good Faith Mortgage, and his wife, who is also in the mortgage industry, have trimmed their household budgets as much as they can to stay nimble.

Kovac sold his truck, which saves him about $1,200 a month, and cut many subscriptions such as Amazon Prime and Netflix, to lower monthly expenses. He said he also had to cancel multiple trips, including flights back home to Chicago for his stepfather’s birthday and for his best friend’s wedding, and to Mexico City for his wife’s grandfather’s funeral.

Aside from the mortgage on his current home, he also is paying off about $44,000 in student loan debt.

He’s also exploring different ways to make money, from sharing some of his expertise on social media, and writing a blog.

But it’s tough, since he’s self-employed and business is down. When he was previously with a bank, while he said he had less freedom, he at least was drawing on a steadier salary and had medical benefits.

Nowadays, clients are getting frustrated as rates fluctuate, sometimes multiple times a day, Kovacv said.

By the time a client gets pre-qualified for a mortgage, looks for a house, and comes back to the lender a couple of weeks later, rates would have gone up, and he’d have to break the news to them.

“And when I provide that new updated pre-qualification letter, they’re like, ‘Whoa, why is the interest rate so much higher?’ It’s almost like they think that we’re playing some sort of bait and switch, which is not the case,” he said.

Competing with home builders and the deals that they’re throwing at home buyers has been another struggle. Many builders have offered rate buydowns, offered to pay closing costs, among other incentives, to entice buyers to purchase a home.

“Any time I pre-approve a client and then they come back and give me a contract and it’s from a builder, I know with 99% certainty that I’m losing that deal,” Kovac said, “because there’s no way any lender can compete with what they’re offering.”

While 2022 has been a “scary” year for Kovac, he’s hoping 2023 will bring him better fortunes as his family navigates the vagaries of mortgage rates.

“We don’t know what the future holds for us… we’ve just been holding our breath all year,” Kovac said, “because there’s so much uncertainty in the industry, that’s been leading to uncertainty in our personal finances.”

We want to hear from readers who have stories to share about the effects of increasing costs and a changing economy. If you’d like to share your experience, write to readerstories@marketwatch.com. Please include your name and the best way to reach you. A reporter may be in touch.

Comments are closed.